Mortgage in Spain – How to Finance a Property in Spain

Dreaming of owning a home in Spain? If you’re considering buying property, you can also apply for a mortgage from a Spanish bank. This can be a great option, especially if you have savings for a down payment and a stable income— but lack sufficient collateral to secure a loan from your bank in your home country. Fortunately, it’s entirely possible—and often quite straightforward—to get a mortgage directly from a Spanish bank.

Who Can Get a Mortgage in Spain?

Foreigners and non-residents (people who live permanently outside of Spain) can apply for a mortgage and finance up to 60-70% of the property’s purchase price. In these cases, the property being purchased serves as the loan collateral. When applying for a mortgage from a Spanish bank, you can trust that the bank will thoroughly review the property. They will ensure it has no outstanding debts or encumbrances and will make sure the ownership is properly registered in your name.

What’s Required to Get a Mortgage in Spain?

To apply for a mortgage in Spain, you’ll need a regular source of income and documentation to prove it. In general, your mortgage payments should not exceed 30% of your net income. Most banks will request the following:

• Income tax returns from the past two years

• Payslips from the last three months

• Bank statements proving income

• Credit report and certificates of assets and liabilities

How Much Down Payment Do You Need?

It’s wise to reserve around 40–45% of the total purchase price to cover the down payment and additional purchase-related costs. These extra costs typically amount to 10–14%, depending on whether it’s a resale or new-build property. This includes transfer tax, notary fees, and registration costs.

Example: If you’re buying a €100,000 property and receive a 70% mortgage (€70,000), you’ll need to cover the €30,000 down payment plus an estimated €10,000–€14,000 in other costs—meaning you should prepare to contribute about €40,000–€44,000 from your own funds. It’s always better to overestimate than underestimate your budget.

Mortgage Interest Rates in Spain (2025)

Variable-rate loans: Usually linked to the 12-month Euribor + bank margin (typically 1–2% depending on the property and client profile)

Fixed-rate loans: Currently available at around 2.5%

Interest rate offers are often tied to additional products such as home or life insurance through the bank

Note: Loan terms and fees vary case by case.

Other Costs to Keep in MindOpening fee: Typically around 1% of the loan amount

Early repayment fee: Some banks charge a penalty for early repayment

Loan transfer to another bank (subrogación): May involve additional costs—negotiate these down if possibleInsurance: Banks usually require home insurance and sometimes life insurance from the same bank

Property valuation (tasación): Around €500 depending on the property size

The Mortgage Application Process

Get a pre-approval: This should be done before property hunting. We help our clients get preliminary mortgage offers from trusted banks.

Property valuation (tasación): The bank arranges an official appraisal through a valuator certified by the Spanish Central Bank.

Final loan approval: Based on the lower of the two—purchase price or appraised value of the property.

Notary meeting: The mortgage contract is signed at the notary during the closing. At this time, the mortgage is also registered as a lien on the property.

Need Help with Financing a Home in Spain?

We support our clients throughout the entire mortgage process - from the first steps to signing the final agreement. We collaborate with several reputable Spanish banks. A rejected application doesn’t always mean the end. In many cases, the issue is simply missing documents or a misunderstanding—things that can be fixed. We’ve helped many eligible clients get approved once everything was properly prepared.

We also assist investors with arranging financing for investment properties. If you ever want to chat about how to finance your future home in Spain, just reach out—I'd love to help!

📩 Laura Stevens✉️ info@costadreamhouse.com📞 +34 681 307 795

Costa del Sol: A Lifestyle Asset for All Generations - buy property in Spain

The Costa del Sol is no longer just for retirement. Today, younger generations are discovering that a home here is a fantastic lifestyle asset, offering a life of health, activity, and balance as...

more

International & Private Schools on the Costa del Sol, Spain

If you’re relocating to Southern Spain with children, finding the right school is likely at the top of your list. The region offers a wide range of international and private schools that...

more

BEST NEW BUILDS IN EL HIGUERON - NEW PROPERTIES FOR SALE

On the border between Fuengirola and Benalmadena lies an area called La Reserva de Higuerón. The area is characterized by modern new construction, which combines Andalucia and Western vanguardism....

more

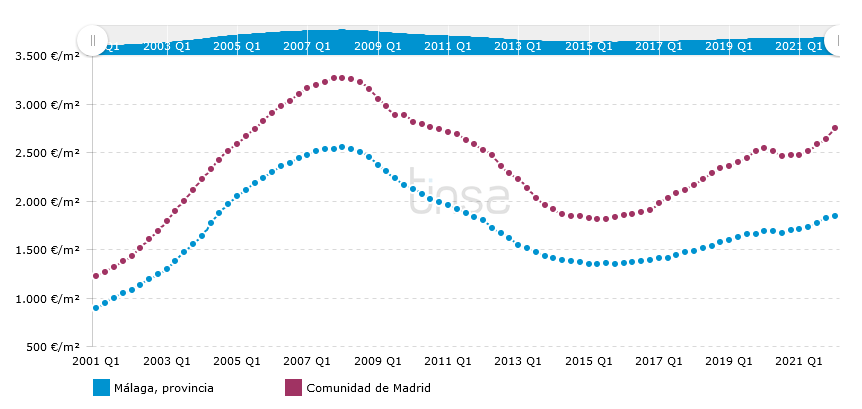

Spanish Property Market Insights Q1 2022

Demand in the Spanish housing market continues to be strong. Buyers are...

more